In the past, dealing with financial products and services in Turkey as a consumer has left me with a bitter taste. I realized the clear lack of tools to manage and improve one’s financial health during my early years of working at the Credit Bureau of Turkey. In the following years, I moved to the U.S. to help Pave build equitable finance for the US consumers, especially for the underserved. As an immigrant with no US credit history, I was also part of the very market I was working to support. After years of analyzing American consumers’ cashflow data to help fintech companies create personalized financial solutions, and using some of the very same tools to improve my own financial health, I’ve come to appreciate the value of open banking for building a more inclusive financial system.

Enter Open Banking

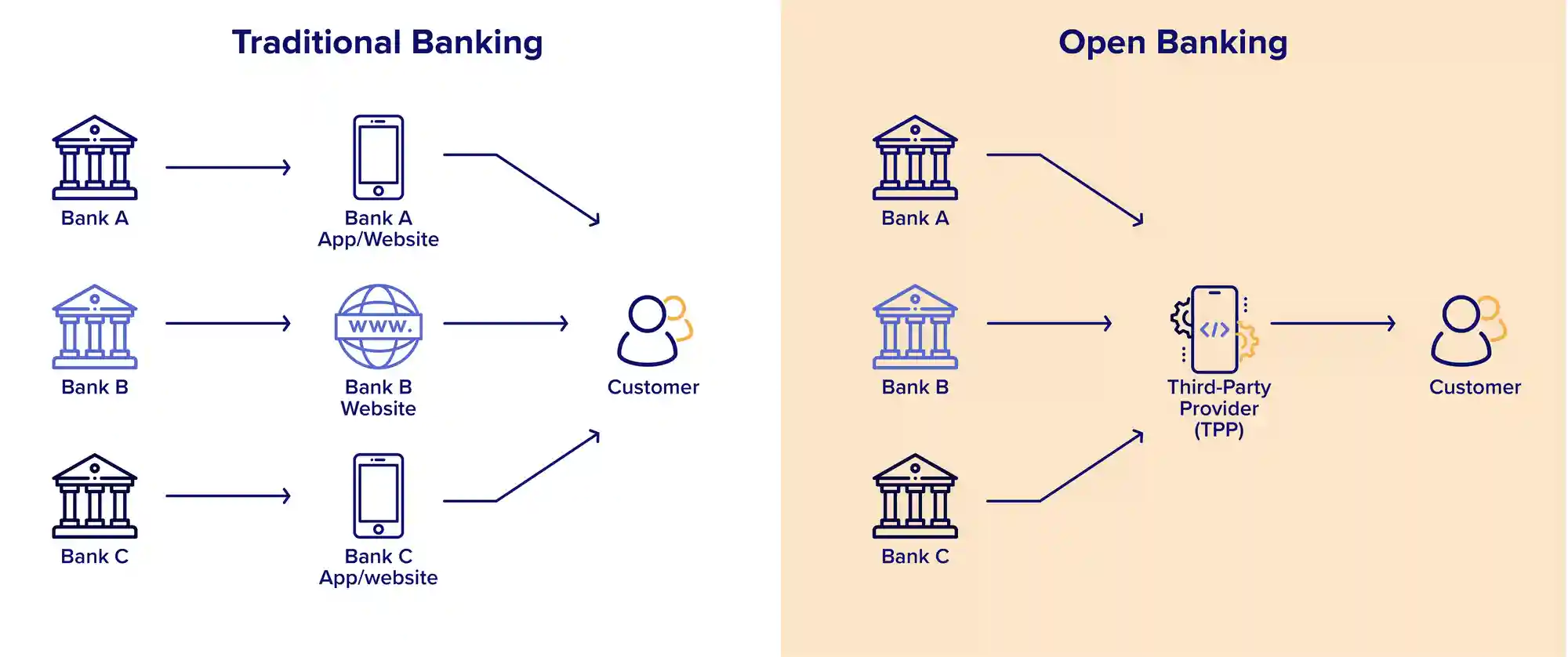

In traditional banking, individuals and businesses must interact directly with their bank for services like transferring money, checking balances, or obtaining financial products like loans and credit cards. Access is typically restricted to the bank’s own systems and services.

Open banking allows third-party financial service providers to access bank data and services through APIs with the customer’s consent. For example, a customer could use a personal finance management app to aggregate their bank account data across multiple institutions, giving them a comprehensive view of their finances.

Traditional banking systems, particularly in underserved or lower-income communities, often involve high fees, limited services, and a lack of personalized options. Open banking can help address this by enabling a broader range of financial products to be tailored to individuals’ needs. For example, a consumer with limited credit history might find it difficult to obtain a loan through a traditional bank. However, with open banking, an alternative lender could analyze their broader financial behavior, including income patterns or savings habits, leading to a fairer assessment of their creditworthiness and access to financing.

Moreover, open banking allows customers to choose from a wider range of financial services, especially in underserved regions. Ultimately, open banking drives innovation, and promotes a more inclusive financial landscape, ensuring that more people can access the financial services they need to thrive.

But why banks would want to adopt open banking? Open banking does, at first glance, create the potential for third parties to leverage a bank’s infrastructure to create competition.

By allowing third parties to access banking data, banks can reach a much larger and more diverse financial ecosystem. Rather than being stuck in the traditional model, banks can partner with fintech companies to create new products and services that they might not have the resources to develop on their own. This creates opportunities to expand their customer base by offering more tailored and modern solutions. For instance, banks can integrate with budgeting apps, or offer smoother payment solutions, which they might not have been able to do before.

Banks that embrace open banking can create stronger relationships with customers by offering new, more relevant products and experiences. Instead of losing customers to third-party providers, banks can maintain a role in their financial lives, even if they aren’t the primary service provider for every function.

Banks can also monetize their data by sharing it with authorized third parties, earning fees for facilitating transactions or offering access to data. For example, banks can charge a fee to fintechs for using their APIs or for enabling payment solutions.

On the other hand, collaboration with fintechs can allow banks to offload certain non-core services for cost-cutting, allowing them to focus on their strengths, such as securing customer deposits.

Finally, the key reason is regulatory compliance. For example, the European Union have mandated banks to provide third-party providers with access to customer banking, transaction, and other financial data via APIs.

Open Banking in the U.S.

In 1997, the foundation for open banking in the United States was laid with the creation of the Open Financial Exchange (OFX), developed jointly by Microsoft, Intuit, and CheckFree. OFX provided a technical specification for financial institutions to exchange account and transaction data with personal finance applications like Quicken and Microsoft Money. [1]

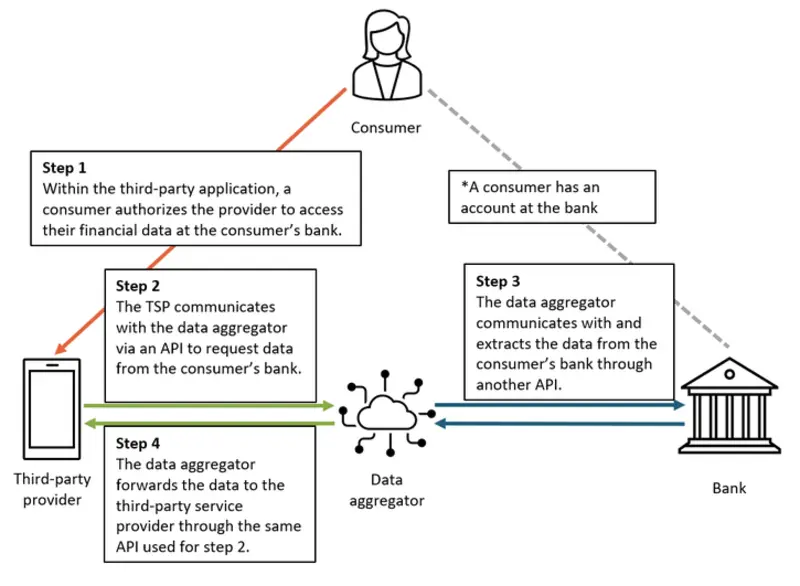

During the early 2000s, data aggregators gained popularity in the U.S. Data aggregators are third-party intermediaries that collect and consolidate users’ financial data across vast amount of sources like banks, credit unions, lenders, brokers, and more. [2]

Especially in their early stages, data aggregators utilized screen scraping to log into users’ bank accounts and extract transaction data without the direct involvement of financial institutions. Companies like Yodlee and Finicity emerged during this time, offering consumers the ability to consolidate their financial information from various accounts, such as checking, savings, credit cards, and investments, into a single, user-friendly platform. While this method allowed for greater financial insight, it also raised concerns about data security and privacy, as it relied on sharing login credentials with third-party services.

Banks and fintech companies began forming bilateral agreements to allow more secure data sharing through APIs. By the late 2010s, industry-led efforts such as the Financial Data Exchange (FDX) emerged to promote API standardization, reducing the reliance on screen scraping, and paving the way for a more secure and structured open banking ecosystem.

The Great Recession marked a crucial turning point for open banking in the U.S. In response to the recession, the congress enacted the federal law known as Dodd–Frank which led to the creation of Consumer Financial Protection Bureau (CFPB) in 2011. Per the law, CFPB’s role is to enforce federal consumer financial protection laws, supervise financial businesses, handle consumer complaints, and educate consumers.

Section 1033 of the Dodd-Frank Act established consumers’ right to access their own financial data and authorize third parties to access it on their behalf upon request. According to the act, CFPB has the authority to issue rules governing how this data should be accessed, shared, and protected.

In 2021, president Joe Biden signed an executive order which called on the CFPB to take action on financial data access under Section 1033 of the Dodd-Frank Act. [3] This was the same year when Plaid settled for $58 million lawsuit due to scraping customers’ bank data and selling the data to third parties without consent. [4]

The CFPB released its rule on Section 1033 in October 2024. With the finalized rule, consumers now have the right to access their account balances, current transactions, 24 months of historical transactions, terms and conditions of the financial institution (fees, APRs, program terms etc.), third party bill payments scheduled through the data provider, basic account verification information, and information to make payments to or from a Regulation E account, including account and routing numbers for ACH transactions. [5]

In 2025, the CFPB has finally officially recognized FDX as a standard-setting organization under its new rule. FDX is now responsible for developing and managing secure standards for sharing financial data, and it must regularly report on how its standards are being adopted. [6] As of 2024, FDX has more than 200 members and reported 76 million consumer accounts utilizing the API. [7]

As of 2024, more than 100 million American consumers authorized a third-party to access their financial data. 45% of US national bank customers already use or are interested in using open banking services. [8]

Looking back, the U.S. has come a long way in open banking. The industry-led initiatives, regulatory support, and consumer demand have driven the adoption of open banking, paving the way for equitable finance for all Americans.

Fintechs in Open Banking

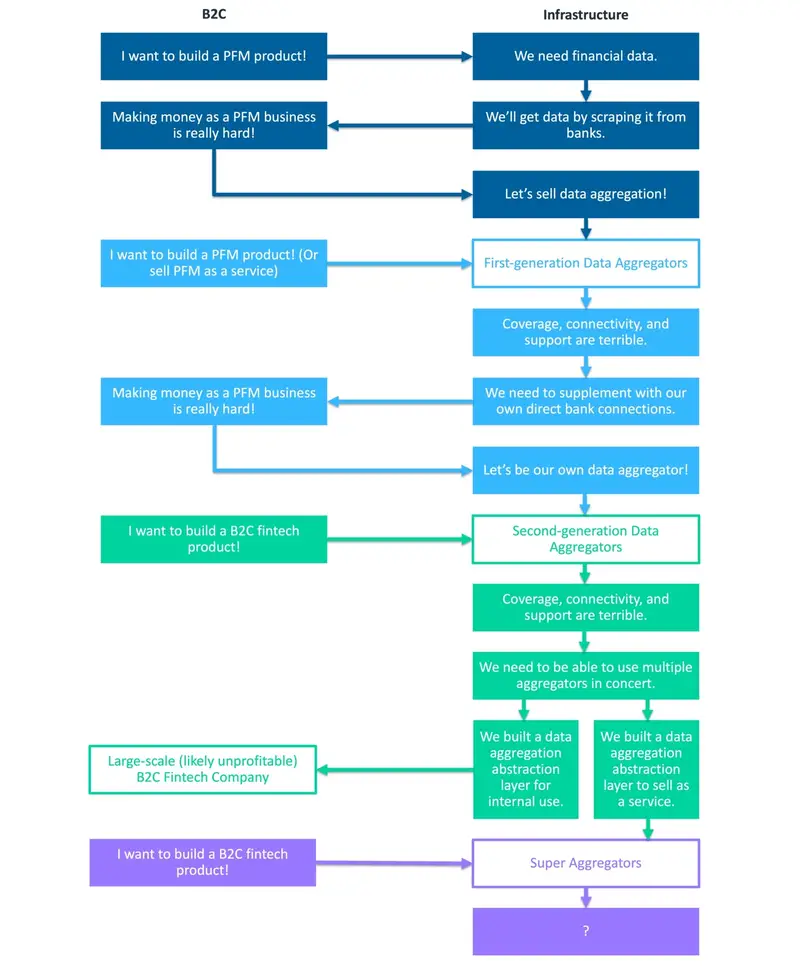

Starting with data aggregators; companies like Plaid, MX, Yodlee, and Finicity provide data aggregation across many financial instutions, facilitate instant account verification, enrich and reconcile transaction data, offer financial health insights and more. Data aggregators are the essential piece for fintech companies to access financial data.

Not every data aggregator has the same financial institution coverage. New fintech startups called super aggregators emerged to solve this problem by integrating with many data aggregators and providing a single unified API for all of them. Some examples are Quiltt, MoneyKit, and Meld. [9]

To be able to build PFM apps, derive financial health insights, or make underwriting decisions from the raw financial data, accurate enrichment and categorization is needed. While some data aggregators like Plaid offer enrichment services, there are also other fintech startups like Pave and Ntropy which are providing dedicated solutions for this challenge. Some examples of the value added at this layer are merchant detection, transaction categorization, and cashflow analytics like recurrence detection, income prediction, rent detection, forecasting overdrafts, and many more.

Using the enriched cashflow data, fintechs provide PFM apps to help consumers manage their finances better. Such apps provide features like account aggregation, bugdeting, expense categorization, subscription management, financial insights, and more. Notable examples are Rocket Money, Intuit Credit Karma, Monarch, YNAB, Quicken Simplifi, and SoFi Relay. PFM and bill pay apps are the most popular top three choices across eight open banking apps in the Mastercard survey of US consumer interest in 2023. Additionally, 73% of US consumers are interested in automated subscription management tools. [8]

Another high-demand use case in which fintechs are starting to utilize cashflow data is lending. Instead of solely relying on traditional credit scores, fintechs are using cashflow and other sources of financial data to underwrite loans. This allows them to provide credit to consumers who may not have a credit history or have a thin file. Some examples are:

- Cash Advance: Small (usually up to $500), short-term, low/no interest fee advances without traditional loan requirements. These help individuals to cover unexpected or necessary expenses before their next payday. Examples: Dave ExtraCash, FloatMe, True Finance, Varo Cash Advance, and MoneyLion Instacash.

- Earned Wage Access (EWA): Allows employees to access a portion of their earned wages before their scheduled payday. Addresses cash flow challenges faced by workers who live paycheck to paycheck, helping them cover unexpected expenses and avoid overdraft fees or payday loans. Examples: DailyPay, Clair, EarnIn, Rain, Payactiv, and Branch.

- Buy Now, Pay Later (BNPL): Allows consumers to split purchases into smaller, interest-free installments, paid over weeks or months. These services are especially popular for online shopping, enabling users to afford higher-cost items by spreading payments over time. Examples: Affirm, Klarna, Afterpay, Sezzle, and Zip.

- Personal Loan: Caters to individuals who need funds for debt consolidation, or large expenses like weddings, home renovation, and medical bills, with flexible repayment terms and lower interest rates compared to credit cards. Examples: Upstart, SoFi, LendingClub, and Prosper.

- Small-Dollar Loan: Short-term, low-amount, unsecured loans to help individuals cover emergency expenses, unexpected bills, or short-term cash flow gaps. Alternative to traditional payday loans, offering faster approval processes, lower fees, and more flexible repayment terms. Examples: LendSwift, Upstart, and PonyMoney.

There are variety of other applications of open banking; neobanks, wealth management, P2P payments, fraud prevention, insurance, and many more.

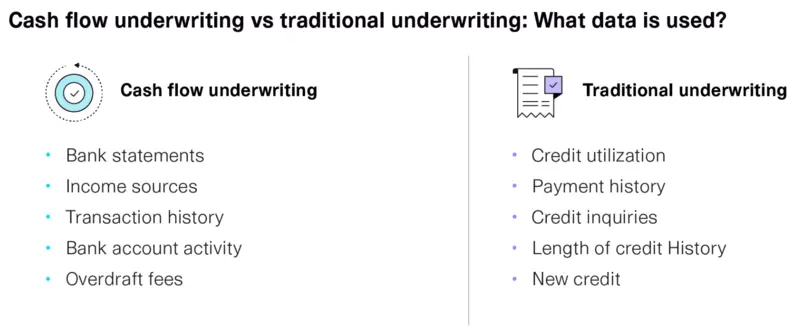

The Case for Cash Flow Underwriting

A large segment of Americans struggle with financial instability, over 125 million adults cannot cover a $400 emergency expense, 76 million work hourly jobs, and nearly 19 million are unbanked or underbanked. More than half live paycheck to paycheck, and many have more credit card debt than savings. [10] Given these challenges, it is not surprising that 55% of US consumers are interested in using open banking solutions to get better loan and interest rates in order to increase their borrowing options. [8]

The U.S. credit system, though extensive, still leaves many potential borrowers underserved. Approximately 50 million consumers in the U.S. lack traditional credit scores, and another 80 million are classified as non-prime, facing higher borrowing costs or outright rejection. Small businesses, particularly startups and minority-owned enterprises, also struggle to obtain financing under traditional models due to insufficient credit history. [11]

The demand for alternative underwriting methods is growing as lenders seek to expand credit access to these underserved markets. Open banking have made it easier for lenders to access real-time transactional data, enabling more accurate and inclusive underwriting models. This shift is particularly significant for gig workers, freelancers, and small business owners who operate outside of traditional employment structures. [11]

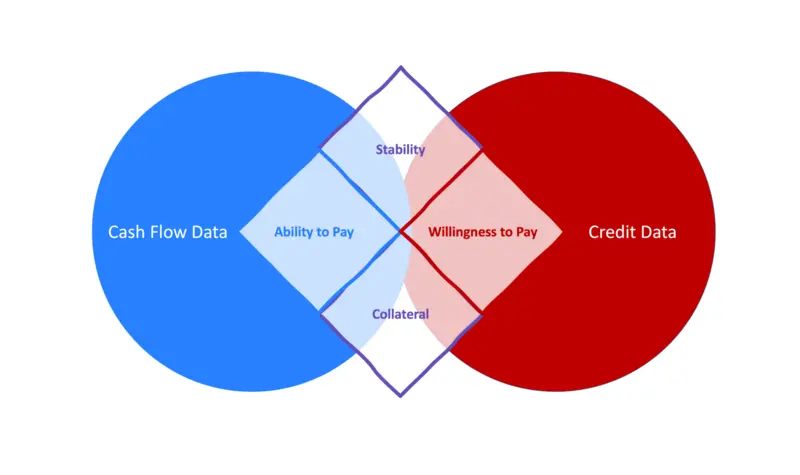

When integrated with traditional credit data, cash flow insights offer a distinct perspective, identifying financial patterns that conventional models often miss. Studies indicate that the correlation between traditional credit scores and cash flow-based scores being very small, confirming that these datasets capture different aspects of financial behavior. [12]

Traditional credit assessments perform well at measuring a borrower’s willingness to pay based on past credit history, but fall short in accurately measuring their ability to pay or their financial stability. Credit inquiries, for instance, are often used as a proxy for financial distress, yet they provide little context. A surge in credit applications could indicate financial trouble, or simply plans for a large expense. [12]

By examining income regularity, spending habits, and available assets, lenders gain real-time insights into a borrower’s financial condition. A sudden drop in direct deposits, for instance, is a clear signal of job loss—far more precise than traditional credit inquiries.

Following this trend, there are a few credit scoring alternatives emering in the US:

- Experian Boost: Looks at qualifying bill payments such as utility, rent, and insurance payments from the connected credit or bank account to boost credit score.

- UltraFICO: Uses information such as age of accounts, recency and frequency of transactions, evidence of consistent cash on hand, and history of positive account balances from the connected checking, savings, and money market accounts to enhance the FICO score.

- Equifax DataX: Collects payment data like checks, cash, money orders, and ACH from third parties to provide credit reports for non-prime and thin-file consumers.

- TransUnion TruVision Resident Credit: A solution for property managers to report their residents’ rent payment information to build incentive for timely payments.

- Nova Credit: Provides FCRA-compliant attributes and a credit risk score for cashflow underwriting using bank transaction data.

- PrismData: Offers cash flow insights and a cash flow-based score to power underwriting decisions.

- TomoScore: A cashflow-based credit score focusing on helping to underwrite high-income individuals without credit history.

- Pave: Provides cashflow attributes, scores, and analytics to help lenders make better underwriting decisions for consumers and SMBs.

The Future of Cash Flow Underwriting

Traditional credit scoring models are not able to account for the nuances of a borrower’s specific financial situation; they often rely on historical data that may not reflect the borrower’s present financial standing or the product they’re seeking. This is where product-specific scores come in, offering a tailored view of a borrower’s ability to repay based on the actual cashflow, rather than a one-size-fits-all metric. [13]

Product-specific scores are designed to evaluate the unique financial characteristics of a particular loan or financial product. These scores take into account factors such as cash inflows and outflows that are directly tied to the product being offered. Imagine a score trained for sole purpose of underwriting cash advances, BNPL, or many other products.

Pave is one of the fintech startups leading the charge in purpose-built scores by providing scores for predicting the likelihood and the ability of paying off credit products like cash advances and personal loans.

Final Notes

Reflecting on my experiences, I’ve seen firsthand the gaps that can exist in traditional financial systems. I think the work I’m doing at Pave, helping build custom-tailored cash flow analytics, is one of the many steps needed to build a more equitable financial future and improve many people’s lives. I’m excited to see how open banking and cash flow underwriting will continue to evolve, and how these innovations will help more people access the financial products and services they need to thrive.

References

OFX Work Group - About,

[Online]. Available: https://www.financialdataexchange.org/FDX/FDX/About/OFX-Work-Group.aspx?a315d1c24e44=1 [Accessed: Feb. 22, 2025].- J. Alcazar and F. Hayashi,

Data Aggregators: The Connective Tissue for Open Banking,

Federal Reserve Bank of Kansas City, 2022. [Online]. Available: https://www.kansascityfed.org/research/payments-system-research-briefings/data-aggregators-the-connective-tissue-for-open-banking/ [Accessed: Feb. 23, 2025]. - ArentFox Schiff, President Biden Issues Executive Order Encouraging CFPB To Act On 1033 Data Access and UDAAP, 2021. [Online]. Available: https://www.jdsupra.com/legalnews/president-biden-issues-executive-order-5700505/ [Accessed: Feb. 22, 2025].

- N. Hanson, Judge approves settlement ordering Plaid to pay $58 million for selling consumer data, 2022. [Online]. Available: https://www.courthousenews.com/judge-approves-settlement-ordering-plaid-to-pay-58-million-for-selling-consumer-data/ [Accessed: Feb. 22, 2025].

- Consumer Financial Protection Bureau, Required Rulemaking on Personal Financial Data Rights, 2024. [Online]. Available: https://www.federalregister.gov/documents/2024/11/18/2024-25079/required-rulemaking-on-personal-financial-data-rights [Accessed: Feb. 22, 2025].

CFPB Approves Application from Financial Data Exchange to Issue Standards for Open Banking,

Jan. 8, 2025. [Online]. Available: https://www.consumerfinance.gov/about-us/newsroom/cfpb-approves-application-from-financial-data-exchange-to-issue-standards-for-open-banking/ [Accessed: Feb. 22, 2025].Financial Data Exchange (FDX) Reports 76 Million Consumers Use FDX API,

[Online]. Available: https://www.financialdataexchange.org/FDX/FDX/News/Press-Releases/Financial_Data_Exchange__FDX__Reports_76_Million_Consumers_Use_FDX_API.aspx [Accessed: Feb. 22, 2025].- T. Angale, G. Racanelli, and R. Menezes,

Orchestrating open banking in the U.S.,

Aug. 20, 2024. [Online]. Available: https://www.mastercardservices.com/en/advisors/data-infrastructure-consulting/insights/orchestrating-open-banking-us [Accessed: Feb. 23, 2025]. - A. Johnson,

Aggregating the Aggregators,

Jun. 14, 2024. [Online]. Available: https://fintechtakes.com/articles/2024-06-14/aggregating-the-aggregators/ [Accessed: Feb. 23, 2025]. - M. Lux and C. Chung,

Earned Wage Access: An Innovation in Financial Inclusion?,

. - The Use of Cash-Flow Data in Underwriting Credit: Market Context & Policy Analysis. FinRegLab, 2020. [Online]. Available: https://finreglab.org/research/the-use-of-cash-flow-data-in-underwriting-credit-market-context-policy-analysis/ [Accessed: Mar. 8, 2025].

- A. Johnson,

Everything You Ever Wanted to Know About Cash Flow Underwriting But Were Afraid to Ask,

May. 22, 2024. [Online]. Available: https://fintechtakes.com/articles/2024-05-22/cash-flow-underwriting/ [Accessed: Mar. 8, 2025]. - A. Shema, Pavefi.com - Power credit decisions with cashflow intelligence, 2024. [Online]. Available: https://www.pavefi.com/blog/the-future-of-credit-scoring-and-how-to-assess-cashflow-scores [Accessed: Mar. 8, 2025].