A Methods of Payment survey conducted in Turkey, revealed that only 7% of the households have basic financial knowledge of interest rates, inflation, and risk diversification. [1] Same research also concluded that as the financial literacy increases, the demand for cash usage at the point of sale decrease. This partly explains why as of 2021, 89% of daily transactions in Turkey are carried out in cash. [2]

The Interbank Card Center of Turkey (BKM) recognized the need to accelerate cashless payment adoption in Turkey. As part of macroeconomic goals for Turkish Republic’s 100th anniversary, BKM’s “Cashless Turkey by 2023” campaign started the year 2012 with the Cards & Payments Trailblazer award for “Best Marketing Initiative”. [3]

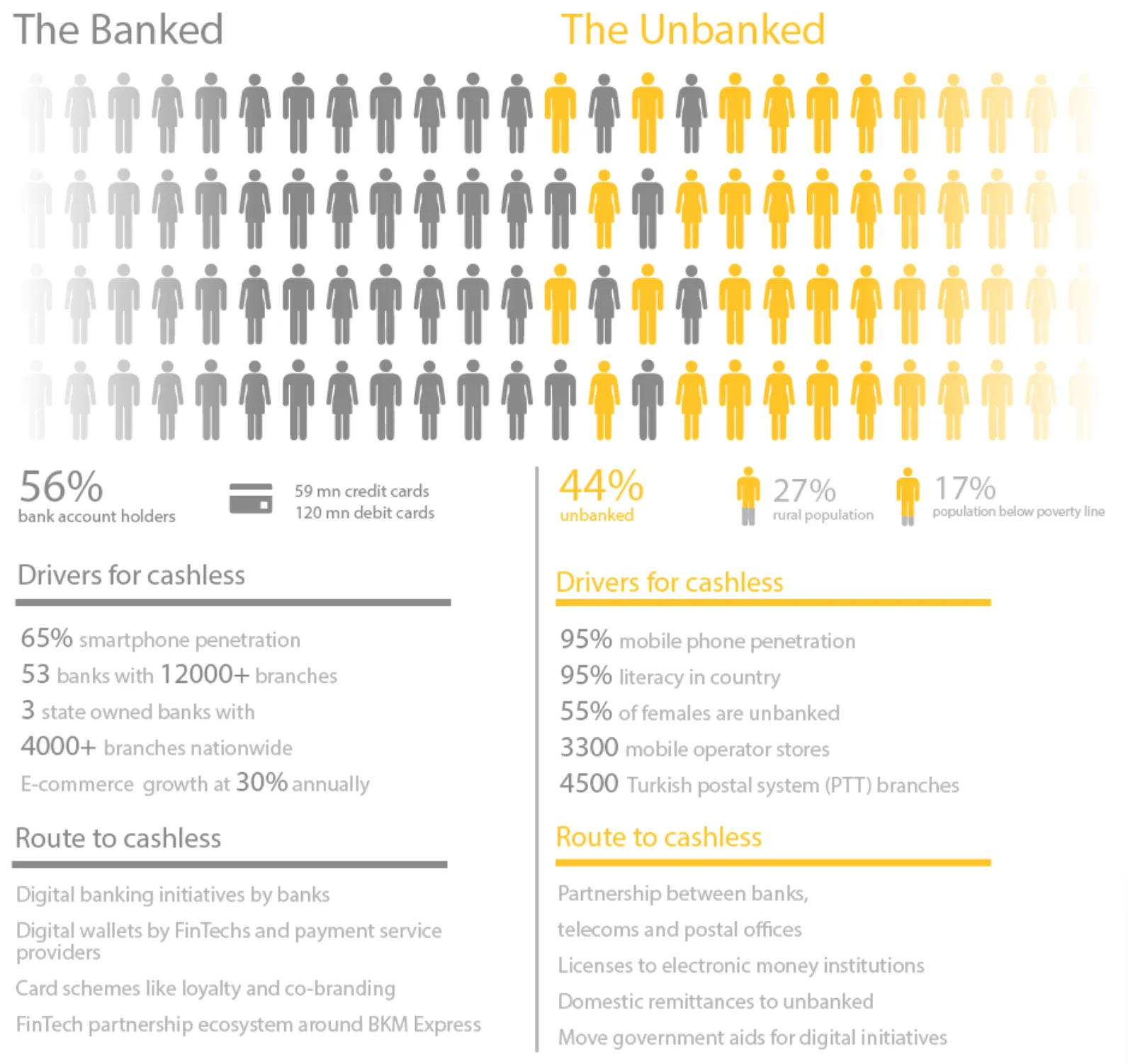

However, as of 2017, BKM highlighted that 44% of the adults (and interestingly, 55% of women) in Turkey are unbanked. The unique challenge in this scenario is driving the adoption of cashless payments for one half of the country while finding ways of delivering basic financial services to the other. [4]

What about the financial institutions? The Turkish finance sector is dominated by a few large banks. The top 7 banks holds 70% of total assets of the Turkish banking system. [5] These banks control essential infrastructure and fintech companies often rely on these banks for access to payment systems and customer data, putting them at the risk of exclusion if banks choose not to cooperate. [6]

Given how established these large banks are, consumers may remain hesitant to transition from traditional banking methods to newer fintech solutions, posing a significant barrier to market penetration for these companies. According to majority of the studies, the biggest deciding factor behind Turkish consumers using online financial services is the perception of trust and security [7], which fintech startups have yet to establish.

The government is also responsible for creating an environment that fosters innovation and competition. Fintech startups in Turkey either face uncertainty due to falling outside of the conventional banking regulatory framework or get blocked by restrictive, costly, and in some cases unfair rules. [6]

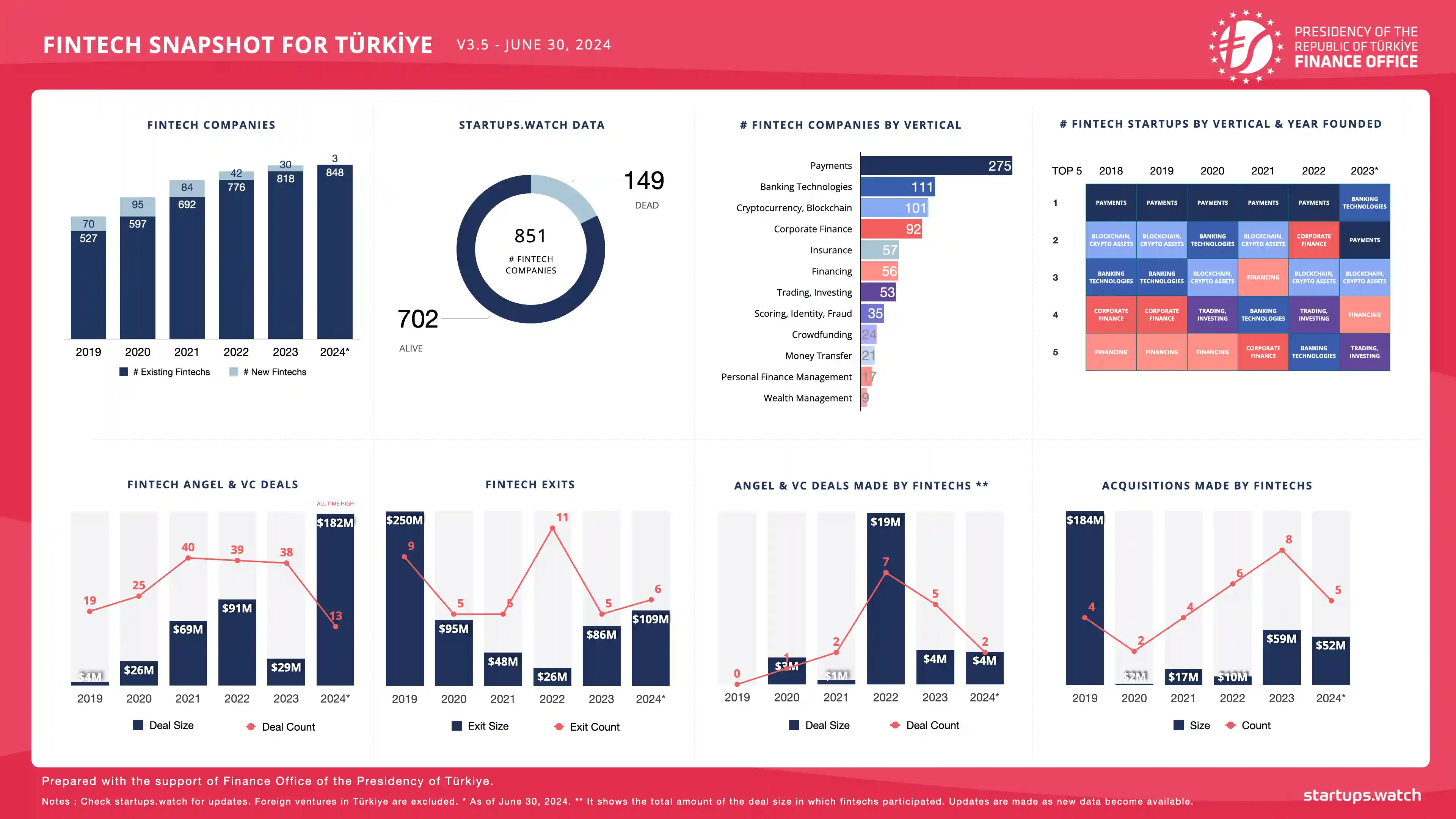

On top of the regulatory hurdles, recent political instability, increasing inflation, and rising currency volatility have made it difficult for Turkish fintech companies. These factors can explain the decreasing number of new fintech startups entering the Turkish market. However, despite all the challenges, Turkish fintech sector is promising for future growth. Record breaking fintech investments of $182 million in the first half of 2024 seems to solidify this sentiment. [8] In addition to funding, improving the regulatory environment and investing in qualified workforce are key for Turkish fintech sector to reach its full potential.

For Turkish fintech startups to capture a complete picture of consumers’ finances, make meaningful improvements to their financial health, and provide solutions for the underserved, companies need the legal framework and technological infrastructure to access wide range of financial data across multiple sources in a standardized way. [9]

Open Banking in Turkey

In 2013, Turkey enacted Law No. 6493 on “Payment and Securities Settlement Systems, Payment Services, and Electronic Money Institutions,” aligning with the European Union’s Payment Services Directive (PSD). This law laid the groundwork for open banking by introducing payment services and electronic money institutions into the Turkish financial system.

According to the Law, electronic money is a digitally stored monetary value issued in exchange for funds, enabling payments without traditional methods and accepted by entities other than the issuer. Electronic money institutions are legally authorized entities that issue electronic money and operate as payment service providers under the law. Other entities according to the Law are payment institutions which are licensed to provide payment services but cannot issue electronic money, extend credit, or engage in other commercial activities. [10] A successful example of electronic money institutions is Papara, which is the first non-bank to issue a Mastercard branded pre-paid card in Turkey.

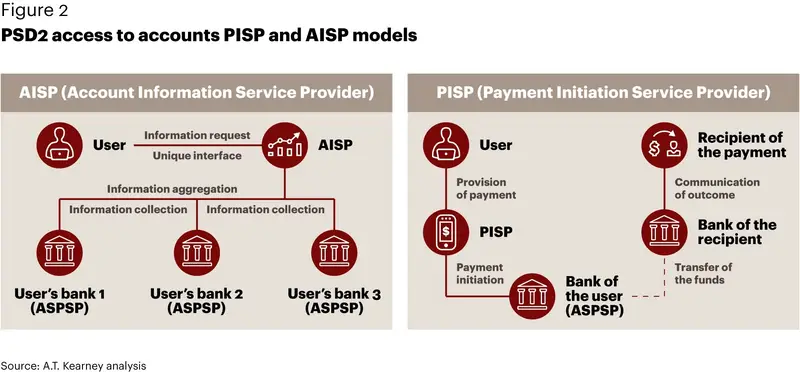

In 2019, Turkey introduced key amendments to its payment services framework, expanding the scope of Law No. 6493 to include Payment Initiation Service Provider (PISP) and Account Information Service Provider (AISP). These amendments allowed third-party providers (TPPs) to initiate payments directly from customers’ payment accounts (PISP) and aggregate information across multiple payment accounts to offer consolidated financial insights (AISP), all with customer consent. [11]

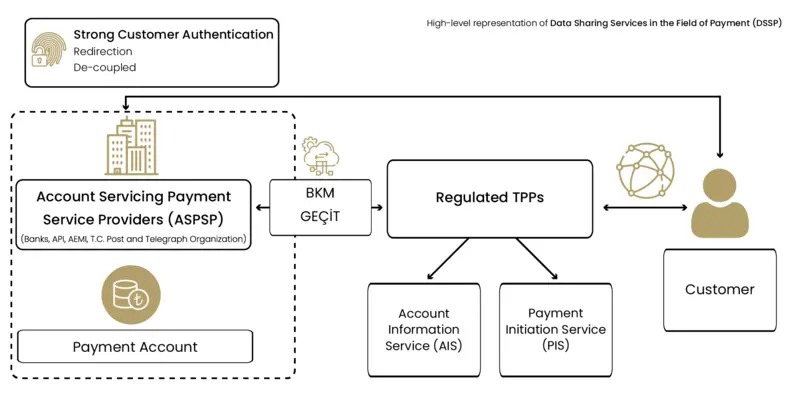

In December 2022, under the supervision of the Central Bank of the Republic of Turkey (CBRT), BKM launched the Open Banking Gateway (GEÇİT). GEÇİT is an API infrastructure standard to carry out open banking services in the payments sector. It enables authorized TPPs to access users’ payment accounts, provided they have explicit consent, allowing for payment order initiation and account information services. [12] According to BKM, there are 19 certified payment service providers as PISP and AISP in Turkey.

Bank executives in Turkey still haven’t fully commit to open banking due to its infancy, lack of business models, and data security concerns. The lack of strategy, ownership and cooperation among banks, fintechs, and regulators are also slowing down the adoption of open banking in Turkey. [13] Even though GEÇİT is a big step in the right direction, Turkey has more work to do to fully embrace open banking.

References

- M. Bilici and S. Çevik,

Financial literacy and cash holdings in Türkiye,

Central Bank Review, vol. 23, no. 4, p. 100129, 2023. doi:10.1016/j.cbrev.2023.100129 - S. Cevik and D. Teber,

The Determinants of Consumer Cash Usage in Turkey,

Working Papers, 2021. [Online]. Available: https://ideas.repec.org//p/tcb/wpaper/2135.html [Accessed: Feb. 12, 2025]. - V. Staff, BKM takes on cash with pro-debit card campaign, 2012. [Online]. Available: https://www.electronicpaymentsinternational.com/uncategorized/bkm-takes-on-cash-with-pro-debit-card-campaign/ [Accessed: Feb. 14, 2025].

- Cashless Turkey by 2023. Interbank Card Center of Turkey (BKM), 2017. [Online]. Available: https://www.burnmark.com/uploads/reports/Burnmark_Report_BKM_Turkey1.pdf

- Bank For International Settlements, Assessment of Basel III risk-based capital regulations - Turkey, 2016. [Online]. Available: https://www.bis.org/bcbs/publ/d359.pdf

- G. Gürkaynak, D. Yeşilyaprak, Z. Ayata Aydoğan, and E. Berkay Kiltan,

The Unstoppable Rise of Fintech and the Competing Efforts of Authorities to Catch Up: The Turkish Competition Authority published its Analysis Report on Fintech,

Feb. 15, 2022. [Online]. Available: https://www.legal500.com/developments/thought-leadership/the-unstoppable-rise-of-fintech-and-the-competing-efforts-of-authorities-to-catch-up-the-turkish-competition-authority-published-its-analysis-report-on-fintech/ [Accessed: Feb. 14, 2025]. - İ. Yıldırım,

Internet Banking and Financial Customer Preferences in Turkey,

in Online Banking Security Measures and Data Protection, IGI Global, 2024, pp. 40–57.doi:10.4018/978-1-5225-0864-9.ch003 - Türkiye Fintech Snapshot – June 2024. Finance Office of Presidency of the Republic of Türkiye, 2025. [Online]. Available: http://www.cbfo.gov.tr/en/news/turkiye-fintech-snapshot-june-2024-prepared-under-coordination-finance-office-presidency [Accessed: Feb. 16, 2025].

- The Fintech Market in Turkey – The Current State of the Fintech Sector And Its Potential to Contribute to Financial Inclusion and Health. Microfinance Centre, 2019. [Online]. Available: https://mfc.org.pl/the-fintech-market-in-turkey-the-current-state-of-the-fintech-sector-and-its-potential-to-contribute-to-financial-inclusion-and-health/ [Accessed: Feb. 15, 2025].

- L. Özer,

Electronic Money and Payment Institutions in Turkish Law,

Dec. 21, 2023. [Online]. Available: https://kilinclaw.com.tr/en/electronic-money-and-payment-institutions-in-turkish-law/ [Accessed: Feb. 16, 2025]. - E. İnal and E. Naz Boyacıoğlu,

FinTech in Turkey: Overview,

Feb. 2020. [Online]. Available: https://www.nortonrosefulbright.com/en-us/knowledge/publications/86be2daf/fintech-in-turkey-overview [Accessed: Feb. 16, 2025]. TCMB - Open Banking Press Release (2022-48),

Dec. 1, 2022. [Online]. Available: https://www.tcmb.gov.tr/wps/wcm/connect/EN/TCMB%2BEN/Main%2BMenu/Announcements/Press%2BReleases/2022/ANO2022-48 [Accessed: Feb. 22, 2025].- Open Banking in the World and in Turkey - The Future of Banking. FinTech Istanbul, 2020. [Online]. Available: https://bkm.com.tr/wp-content/uploads/2015/06/open_banking.pdf [Accessed: Feb. 16, 2025].